30 Giga-Watt Hours of Electric Vehicle Markets Beyond Cars, Reports IDTechEx

Electric vehicle markets are growing globally - in total IDTechEx's latest master electric vehicle report "Electric Vehicles: Land, Sea & Air 2022-2042" finds 35.7 million electric vehicles (EV) were sold in 2021 and predicts this will rise to over 74 million by 2030.

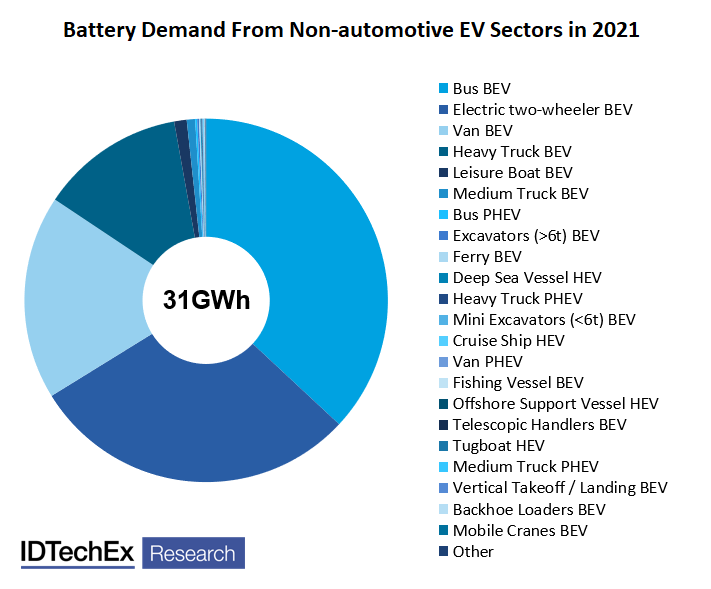

While electric cars will remain the largest electric vehicle market for the foreseeable future in terms of battery demand and market revenue generation, most transport sectors are facing a transition. In this article, IDTechEx summarizes key developments in non-automotive sectors, showing each sector's global battery demand (in 2021) for relative scale. For reference, battery-electric and plug-in hybrid cars demanded approximately 280GWh globally in 2021.

Battery Demand From Non-automotive EV Sectors in 2021. Source: IDTechEx - "Electric Vehicles: Land, Sea & Air 2022-2042"

Electric Air Taxis/ Electric Vertical Take-off & Landing (eVTOL) - <<1GWh

The future of electric air taxis, or electric vertical take-off and landing (eVTOL), is perhaps the most uncertain due to high regulatory barriers as well as technical. This is a low-volume, high-value market where aircraft will rely on high-cost and cutting-edge technologies to reach new heights with regard to performance and safety. For example, IDTechEx expects that lithium-metal and solid-state batteries, axial flux motors, and carbon fiber materials will play an important role in eVTOL markets.

From IDTechEx's review of the most promising eVTOL companies, 21 have presented timeline information about when they are looking to begin commercial eVTOL production, plans which are highly dependent on flight certification. Several companies have said they are a couple of years into what they think will be a five-year certification process. However, the certification standards are not yet fully in place, and significant technological and funding issues create uncertainty. Most eVTOL manufacturers are targeting 2023 for the start of commercial operations, and the IDTechEx report provides forecasts in unit sales and battery demand through 2042.

Electric & Hybrid Marine - <1GWh

In the commercial marine sector, batteries are starting to saturate early adopter segments, such as ferries, and reach their limitations in others, such as the short and deep-sea vessels (which produce the majority of the sector's emissions). While battery demand will still grow - the addition of a battery to any powertrain for load management is generally beneficial - it cannot be the sole solution in seagoing sectors.

Meanwhile, policy focus is shifting from localized emissions to greenhouse gases, with new technical and operational ship requirements coming in from 2023. Upcoming IMO policy includes an 'Energy Efficiency Existing Ship Index (EEXI)' and the Carbon Intensity Indicator (CII). EEXI ensures a ship is taking technical steps, in terms of how it is equipped and retrofitted, to reduce greenhouse gas emissions. CII is a measure of the carbon emissions per amount of cargo carried per mile and targets reducing emissions operationally. The measures are expected to become mandatory from 2023, with the first ship ratings given in 2024.

The new regulations are driving interest in e-fuels, ammonia, and hydrogen as the industry scrambles to find multiple silver bullets. Indeed, fuel cell projects are gathering momentum, with system deliveries ranging up to 3.2MW and some potential supplier order pipelines reaching 200MW. Most projects thus far have been for inland vessels and some short-sea vessels. The greatest challenge is the same as that which is plaguing the adoption of fuel cells in the automotive market - the buildout of low-cost green hydrogen infrastructure.

Electric Vehicles in Construction - 1GWh

There are relatively few strong market drivers for electric vehicles in construction. Broader commitments to climate change are spurring some countries, like Norway and Holland, or companies, like Volvo, to set their own targets. Health and safety concerns, like the impact of diesel particulate exhaust emissions on construction worker health, and noise, could be equally important drivers. Yet, much of the early electric construction vehicle development has been through retrofitting, a necessary development phase but not an economically sustainable strategy in the long term. OEMs need to design large EVs from scratch and manufacture at volume to realize economy-of-scale savings.

The largest construction machine market sectors in twenty years are Mini-Excavators, Excavators, and Loaders, but electrification development is initially focused on smaller compact machines (mini-excavators/compact loaders). These have comparatively short operating hours and low energy consumption, which explains the relatively low battery demand today (~1GWh). Like maritime markets, overall, most emissions are generated by the heavy excavator segment, which is, therefore, an important sector to electrify.

Electric Trucks - 4.3GWh

Tesla, Daimler, VW, and Volvo are all investing heavily in battery-electric trucks. Tesla is famous for announcing a battery-electric long-haul class 8 truck, with CEO Elon Musk recently stating that its first deliveries will be to Pepsi by the end of 2022. While there are far fewer trucks than cars globally to convert to electric, they use much larger batteries (several hundred kWh) and accounted for 4.3GWh annually in 2021.

A smaller minority - Toyota, Hyundai, and Nikola - have chosen to focus their efforts on fuel cell trucks as the powertrain of the future. Despite issues with the efficiency and cost of hydrogen as a fuel, FCEV remains in the conversation as a technology for long-haul trucking applications, where a greater range is required, though the viability of this technology is dependent on the production of low-cost green hydrogen.

Today, city trucks in China are predominantly hitting the roads as Chinese manufacturers leverage their experience in electric buses and battery production. Given the Chinese government's strong support for the entire EV industry, it is likely that this is where the most significant deployment of EV trucks will be seen in the following years. As the increasing numbers of cities and nations around the world phase out of diesel and petrol-fuelled vehicles by 2030 and the cost benefit and ability of the technology to deliver the required daily duty cycles are demonstrated, the electrification of truck fleets is likely to happen rapidly.

Electric Two-wheelers - 9GWh

Sales of electric two-wheelers have long been dominated by the approximately 25-30 million annual unit sales of low powered lead-acid battery electric two-wheelers in China, but this is a saturated market. Historic growth outside of China is driven by Europe and India, markets affected by the pandemic in 2020 but which recovered in 2021.

Often, two-wheelers are the low-hanging fruit when it comes to electrification. With small batteries typically under 4kWh (compared to over 50kWh for a battery-electric car), they have a relatively low upfront cost to consumers and lend themselves to new business models such as battery swapping. Electrification of two-wheeler markets, for example, of the 15 million annual motorcycle sales in India, is key to reducing pollution in countries where the car is not the dominant transportation mode. Overall, Li-ion battery demand for electric two-wheelers in 2021 was 9GWh, and IDTechEx expects this to grow rapidly as China transitions from lead-acid and growth accelerates in other parts of the world.

Electric Buses - 12GWh

Tier 1 cities in China were the first to adopt electric buses, driving rapid growth between 2012-2016, but now many of these markets are saturated. In 2018, Beijing and Shanghai had 9,368 pure electric buses constituting 55% of the combined fleet, all initially powered by a 50% purchase subsidy. The saturation of Tier 1 cities in China has caused global electric bus sales to decline for the past five years, offset only slightly by growth from Tier 2 and 3 cities in China. Today, subsidies have been greatly reduced.

Future growth in the near term is driven by Europe. The European electric bus market is highly fragmented and, over the past few years, has relied on Chinese OEMs, which still accounted for a quarter of unit sales in 2021 - in fact, BYD and Yutong have consistently been market leaders since 2019. A local supply chain underpinned by European OEMs will be key and will slowly drive mid-term growth in global electric bus markets up from 12GWh.

IDTechEx Research

To learn more, please see the IDTechEx report "Electric Vehicles: Land, Sea & Air 2022-2042" (www.IDTechEx.com/EV).

This research forms part of the broader electric vehicle and energy storage portfolio from IDTechEx, who track the adoption of electric vehicles, battery trends, and demand across land, sea and air, helping you navigate whatever may be ahead. Find out more at www.IDTechEx.com/Research/EV.