Given the rapid increase in forecast demand for Li-ion batteries, there has been significant growth in the number of gigafactories being planned and announced over the past 2-3 years. IDTechEx analysis shows that current plans and announcements for new cell production capacity will reach 3 TWh by 2030. While this would not meet forecast demand, the relatively short time period needed to build new cell production factories allows time for the additional investment and expansion needed to meet forecast demand from EVs. Nevertheless, continued growth is required.

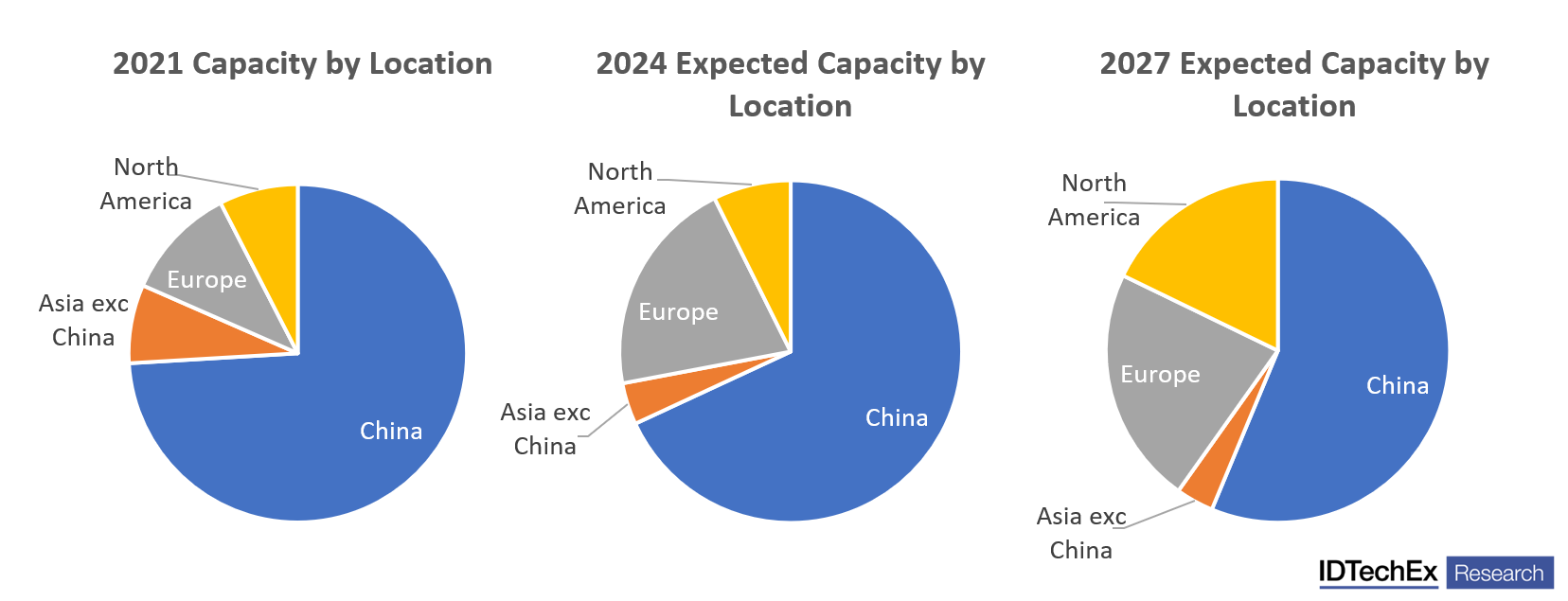

China and Asia have dominated the cell and battery manufacturing market, but the industry is seeing a shift toward the localization of Li-ion battery manufacturing. As the demand for electric vehicles and renewable energy storage increases, countries are recognizing the benefits of having local battery manufacturing capabilities. This helps to ensure the security of supply and reduce dependence on imports, as well as creating jobs and supporting local economies. Europe is expected to grow its share of manufacturing capacity to 22% by 2027, up from approximately 11% in 2021, while US manufacturing capacity is expected to grow to 18% of global capacity from approximately 7% in 2021.

Capacity by location. Source: IDTechEx - "Li-ion Battery Market 2023-2033: Technologies, Players, Applications, Outlooks and Forecasts"

Much of this growth has been driven by incumbent manufacturers such as CATL, BYD, LG Energy Solution, SK Innovation, and Samsung SDI. Auto OEMs in Europe and the US are also looking to enter into joint ventures to secure supply and expertise in this critical component for EVs. For example, Ford and SK Innovation, GM and LG, and Samsung SDI and Stellantis have entered into agreements for production in the US, while in Europe, ACC was formed between Saft and PSA Group, Northvolt and VW have also into partnerships for cell production.

Start-ups and early-stage companies are also looking to enter the market, especially in Europe but also the US. Northvolt, Freyr, iM3NY, Verkor, InoBat, Phi4Tech, and Italvolt are just some examples of younger companies and ventures looking to enter the battery race. Difficulties in acquiring the equipment and tools for manufacturing lines, starting-up operations and managing scrap rates, and purchasing the raw materials and components, will all impact when new factories come online and the volume of cells manufactured. Some projects have been delayed and project cancellations are also a risk. Britishvolt's troubles in the UK can serve as a warning as to the difficulty of creating a cell and battery manufacturing company from the ground up. Competing with the Asian giants will be challenging. Many of these established companies have enjoyed decades of experience, access to strong domestic markets, especially in China, access to capital, and have developed customer relationships. This can make it challenging for smaller companies or new entrants to establish a foothold in the market and could impact the outlook for European-based manufacturing in particular. Nevertheless, the rapid growth expected and required from the Li-ion industry requires a broad set of players across various regions to be capable of manufacturing the Li-ion batteries that will underpin much of the electric vehicle industry and be key to the adoption of increasing levels of renewables.

To find out more on the Li-ion market, please see the IDTechEx report "Li-ion Battery Market 2023-2033: Technologies, Players, Applications, Outlooks and Forecasts".

This report forms part of the IDTechEx energy storage portfolio. To find out more, please visit www.IDTechEx.com/Research/ES.