The automotive sector is rapidly electrifying, with electric car sales totaling over 5.8 million units in the first half of 2023 across China, Europe, and the US. While automotive electrification is at the forefront of the public eye, other vehicle sectors also present huge opportunities, with IDTechEx predicting the global market of electric vehicles for land, sea, and air to be worth over US$1 trillion in 2044 (excl. automotive).

IDTechEx's report, "Electric Vehicles: Land, Sea, and Air 2024-2044", provides historic performance and granular forecasts of unit sales, battery demand, and market value for electric vehicle markets, including cars, buses, vans, trucks, two-wheelers, three-wheelers, microcars, boats & ships, construction, trains, and air taxis (eVTOL).

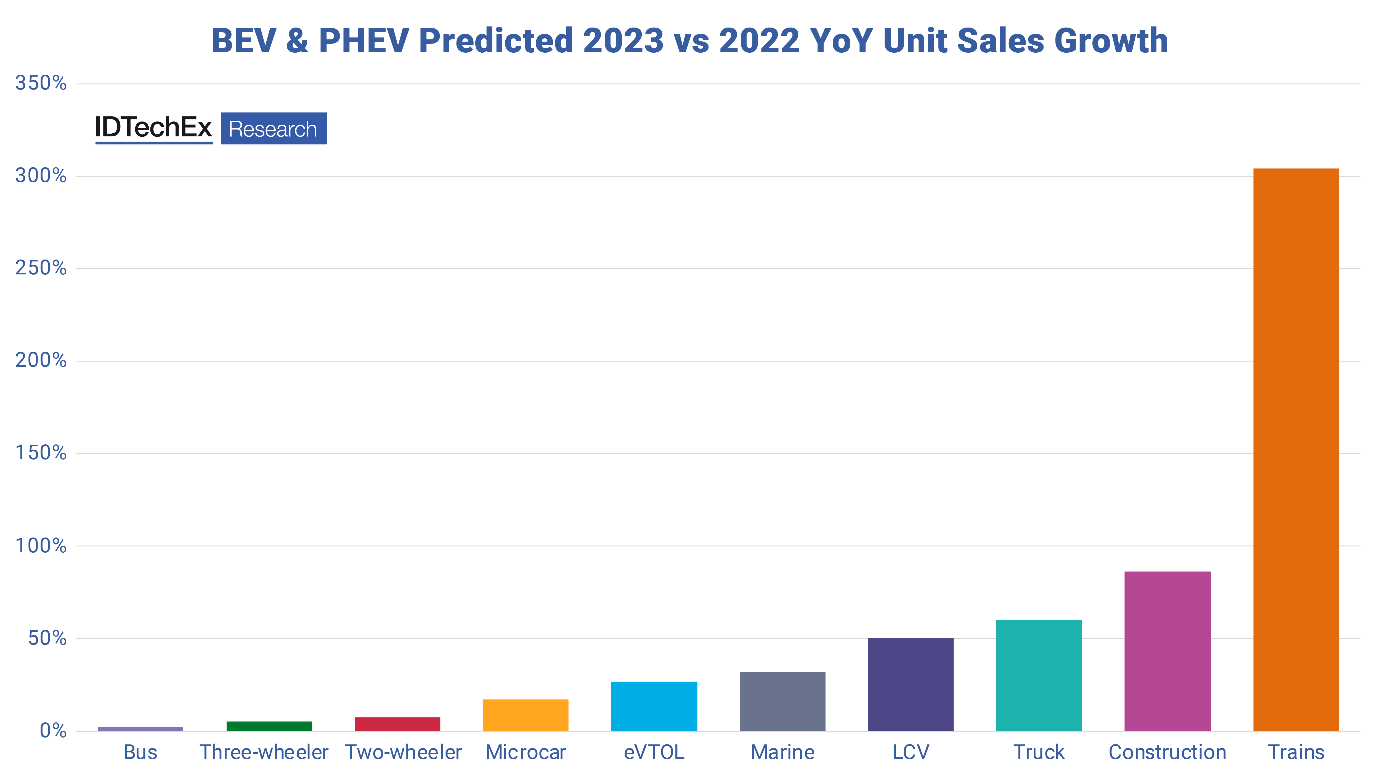

All categories outside of cars are also rapidly electrifying. Source: IDTechEx

Commercial Vehicles (Vans, Trucks, Buses)

Commercial vehicles are deployed in smaller volumes than automotive but are also heavily electrifying and an important stage in global emission reduction. These markets are at an earlier stage of electrification but are making significant progress.

Electric buses presented an early market in China. IDTechEx predicts that due to the saturation of China's electric bus market, global sales will not surpass their 2016 peak until 2040, with future growth fuelled by replacements in China and greater adoption in Europe. Much of the European market has been underpinned by Chinese OEMs, but local supply is now starting to ramp up.

Electrification of light commercial vehicle (LCV) fleets is proving to be an effective way to demonstrate green credentials to customers, but also a strong total cost of ownership (TCO) reduction for fleet operators. Significant adoption has been seen from operators like Amazon and UPS. In Europe, the average van OEM has 8% of its new registrations coming from electric LCVs.

Tesla, Daimler, VW, and Volvo are all investing heavily in battery electric trucks. A smaller minority, Toyota & Hyundai, have chosen to focus their efforts on fuel cell trucks as the powertrain of the future. Despite issues with the efficiency and cost of hydrogen as a fuel, FCEV remains in the conversation as a technology for long-haul trucking applications, dependent on the production of low-cost green hydrogen.

There is an increasing number of cities and nations worldwide phasing out diesel and petrol-fuelled vehicles by 2030, and the cost-benefit and ability of the technology to deliver the required daily duty cycles is being demonstrated. The electrification of truck fleets is likely to happen rapidly; electric truck sales in 2022 were 2.2 times that of 2021, showing the start of the exponential takeoff.

MicroEVs (two-wheelers, three-wheelers, and microcars)

In China, India, and several other Asian regions, the two- and three-wheeler is the dominant form of personal mobility. In terms of electrification, these have typically been dominated by lead-acid battery variants. With the small battery size and low motor power required for these vehicles, they can present a relatively low-cost form of electrification.

Electric microcars are an emerging form of transport that has proven especially popular in China, thanks to the lower range requirement needed and the ability to traverse crowded cities more easily than a full-sized car.

The microEV segment currently dominates unit volumes and will remain a large market in the long term. However, its battery demand will be overshadowed in the long run by the rapidly growing electric car market with much larger battery demands.

Electric & Hybrid Marine

The electric boating market has tripled since COVID-19 emerged, as more time away from the office has led to increased interest and free time for leisure boating. While low-power outboard categories are typically two times more expensive than petrol equivalents, the business case is strong from a TCO standpoint alongside other advantages (quiet, clean, etc.). Despite this, high battery prices remain a barrier in higher power outboard or inboard categories. Unlike the automotive market, the industry lacks governmental policy drivers, which have remained largely unchanged for a decade.

Since 2016, the market has started to follow an exponential trajectory for larger commercial electric and hybrid vessels as the industry is less price sensitive and maritime battery prices halved. A strong economic driver emerged in downsizing oversized engines using batteries to power peak loads in short-sea vessels such as OSVs. Ferries are the most common electric vessels as the low-hanging fruit that can opportunity charge and travel shorter and consistent routes. The IDTechEx report provides forecasts for electric leisure boats, short sea commercial vessels, and deep-sea commercial vessels.

Electric Vehicles in Construction

Broader commitments to climate change are spurring some countries, like Norway and Holland, or companies, like Volvo, to set their own targets for electrification of construction equipment. Health and safety concerns like the impact of diesel particulate exhaust emissions on construction worker health and noise could be equally important drivers. Much of the early vehicle development has been through retrofitting, a necessary development phase but not a sustainable strategy in the long term. OEMs need to design large EVs from scratch and manufacture at volume to realize economy of scale savings. The report forecasts that electric construction vehicles will be a market worth approximately US$154 billion by 2044, made up of a low volume of high individual value vehicles. The report explains that the largest construction machine market sectors in twenty years are Mini-Excavators, Excavators, and Loaders, but electrification development is initially focused on smaller compact machines (mini-excavators/compact loaders) that have comparatively short operating hours and low energy consumption.

Electric Air Taxis / Electric Vertical Take-off & Landing (eVTOL)

The timeline for eVTOLs to become commercial is highly dependent on the final certification process in each geographical market. As developmental projects, these timelines should be treated somewhat skeptically; a number of companies have said they are a couple of years into what they think will be a five-year certification process. However, the certification standards are not yet fully in place. Significant technological and funding issues will need to be addressed for many companies before a production eVTOL can be launched. The IDTechEx report covers when the different players expect to become commercial and market forecasts through to 2044.

Outlook

Electrification is at varying stages in each category mentioned above but is growing in each sector. Combining the markets for two-wheelers, three-wheelers, vans, microcars, trucks, marine, construction, buses, air taxis, and trains, IDTechEx's report "Electric Vehicles: Land, Sea, and Air 2024-2044" predicts a market of just over US$1 trillion in the year 2044.

To find out more about this IDTechEx report, including downloadable sample pages, please visit www.IDTechEx.com/EV.

IDTechEx guides your strategic business decisions through its Research, Subscription and Consultancy products, helping you profit from emerging technologies. For more information, contact research@IDTechEx.com or visit www.IDTechEx.com.