Industries have traditionally used fossil fuels to produce heat for their processes or to fuel power plants to generate electricity, including the use of natural gas, oil, and coal. Industrial heating processes are responsible for ~25% of global emissions, and therefore, great attention from governments and states is being seen to decarbonize this area of industry. A key solution that could reduce emissions from industrial heating processes is thermal energy storage (TES). From their new market report, "Thermal Energy Storage 2024-2034: Technologies, Players, Markets, and Forecasts", IDTechEx forecast that over 40 GWh of thermal energy storage deployments will be made across industry in 2034.

While TES will be a key technology to decarbonize industrial heating, players developing other technologies, such as carbon capture and storage (CCUS), heat pumps, hydrogen, and electrification technologies, such as electric arc furnaces (EAF), will also be competing for funding from states and governments. It is, therefore, important to examine the different drivers and initiatives that will influence where the greatest TES market growth is expected to be seen over the coming decade.

Key drivers for decarbonizing industrial heating in Europe

Natural gas prices in Europe have risen in recent years due to geopolitical instances and fears of strikes in key exporting countries. In Europe, natural gas prices have risen and been more volatile in recent years. This is mostly due to the influence of the Russia-Ukraine war, which saw European natural gas prices rise from €10-20 / MWh before 2022 to over €300 / MWh. These prices have seldom returned to prices pre-2021, and other spikes in natural gas prices have been caused by fears of LNG exporter strikes in Australia. This volatility and increase in natural gas prices will likely be a key driver for the growth of technologies to decarbonize industrial heating in Europe, including TES.

The European Commission has enforced the EU Emission Trading System (EU ETS), which sees companies penalized for the emissions they produce above a given cap. This cap will be reduced annually to help ensure that emissions from industry decrease over time. Companies can auction for allowances on the common auction platform, performed on the European Energy Exchange. As companies in the EU are paying for the excess GHGs they emit, they are either able to purchase carbon allowances or, hopefully, are incentivized to invest in technologies to provide low-carbon heat.

The funds gained by the Member States are mostly used to support climate-related endeavors, and from 2013-2019, approximately 78% of the revenues gained were put towards these purposes. This funding is put towards the EU Innovation Fund. In November 2023, the EU Commission opened a €4B fund to support the deployment of decarbonization technologies, building on its previous two rounds of €3B and €1.8B in 2022 and another €1.1B round in 2021. This funding will be used to support decarbonization projects, which could include energy storage technologies, heat pumps, and hydrogen production. As suggested in IDTechEx's market report, players developing thermal energy storage technologies could be eligible for part of this funding, but the volume of funding specifically being provided towards players developing and commercializing TES technologies is unknown.

Key drivers for decarbonizing industrial heating in the US and Australia

TES technologies will be less competitive with natural gas in the US, given that the US has a large volume of domestic natural gas production and is a net exporter. However, in 2022, the US Department of Energy (DOE) launched the Industrial Heat ShotTM Initiative to develop cost-competitive industrial heat decarbonization technologies. In 2022, the DOE announced it would provide a "$70 million funding opportunity" in federal funding over the next five years for developing projections focused on low-carbon process heating technologies. However, in 2022, US$300M was requested by players, and US$385M was requested in 2023, therefore suggesting that demand for funding of low-carbon process heating technology development is greater than what is currently being provided. Regardless, growth of TES technologies in the US is expected, though players developing other decarbonization technologies will compete for funding.

End-user natural gas prices in eastern Australia have typically mirrored those of western Europe. While eastern Australia has its own production of natural gas, domestic liquefied natural gas (LNG) consumption competes against export volumes. Generally, Australia's export volumes are much larger than the total gas demand, and the cost of gas production is high. This will likely see TES technologies be more cost-competitive against natural gas than in the US, to similar levels as Europe. Moreover, in November 2023, The Australian Renewable Energy Agency (ARENA) launched an AU$400M (~US$260M) fund named the Industrial Transformation Stream (ITS). The first round of funding will see AU$150M of funding provided for decarbonization of industrial heating processes and off-road transport decarbonization. TES players in Australia are, therefore, likely contenders to receive this funding.

Thermal energy storage regional market outlook

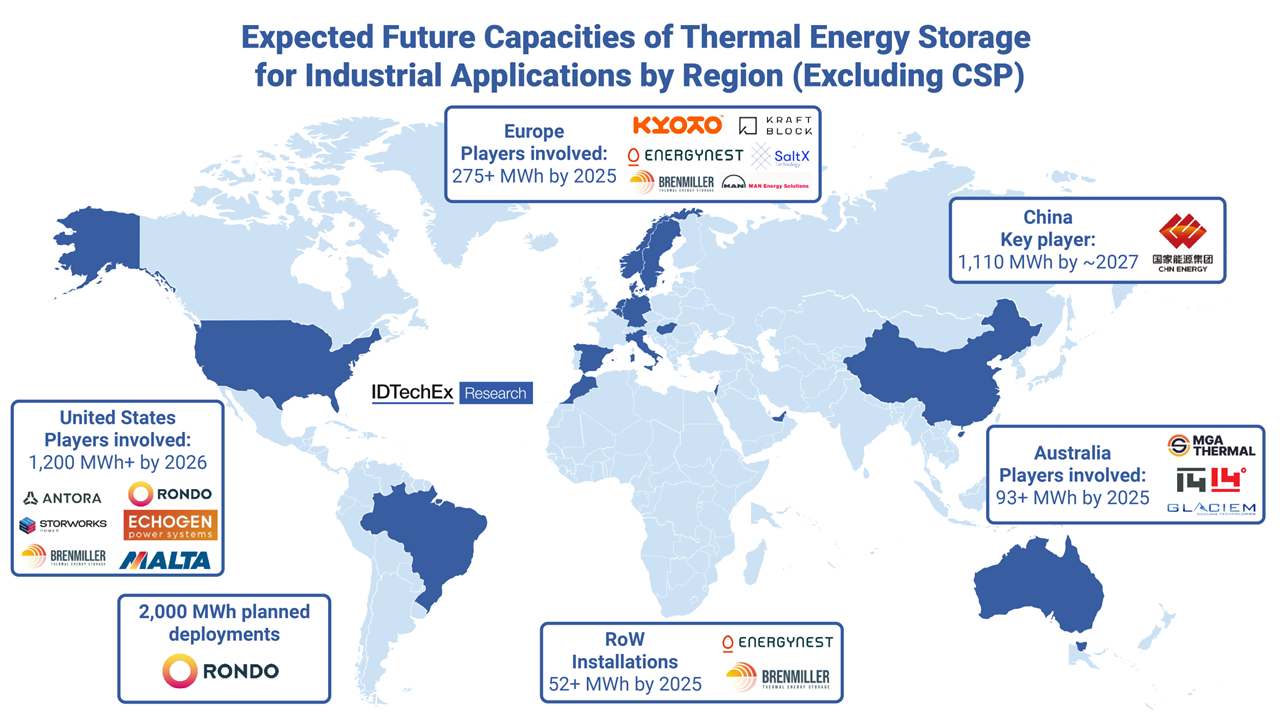

Key players in interviews with IDTechEx have commented that most decarbonization projects are currently using support funds from state or government grants. As detailed in IDTechEx's market report, as of January 2024, TES players have accumulated over US$600M in funding, though not all through state or government grants. Over the next few years, most industrial TES growth is expected to occur in Europe, with over 275 MWh of projects planned for deployment by ~2025. Two key projects in the US and China will see GWh-scale deployments of a 1.2 GWh electro-thermal energy storage (ETES) system by Echogen Power Systems in the US and a 1.1 GWh TES system by CHN Energy at a power plant in China. Rondo Energy is also planning to deploy 2 GWh of TES for industrial heating applications, seemingly across multiple projects, though locations are currently unknown.

Expected future capacities of thermal energy storage for industrial applications by region (excluding CSP). Source: IDTechEx

These deployments skew the outlook from a TES capacity perspective, though the described factors of higher and volatile natural gas prices, the enforced EU ETS, and support from the EU Innovation Fund will be the main drivers creating opportunities for TES market growth in Europe over the next decade. While it is difficult to pinpoint exact volumes of funding being provided for development of TES technologies, it is clear that other countries, such as the US and Australia, are also directly supporting decarbonization of industrial heating, and these will be other key regions for TES growth in the medium-term.

For more detailed information on thermal energy storage technologies and benchmarking analysis, key players, applications, markets, government initiatives, drivers, and granular 10-year market forecasts, please refer to IDTechEx's new market report "Thermal Energy Storage 2024-2034: Technologies, Players, Markets, and Forecasts".

To find out more about this IDTechEx report, including downloadable sample pages, please visit www.IDTechEx.com/TES.

For the full portfolio of energy storage market research available from IDTechEx, please see www.IDTechEx.com/Research/ES.

Related articles:

IDTechEx provides trusted independent research on emerging technologies and their markets. Since 1999, we have been helping our clients to understand new technologies, their supply chains, market requirements, opportunities and forecasts. For more information, contact research@IDTechEx.com or visit www.IDTechEx.com.