Electrification is tough. It has taken around 15 years to convince car owners that battery power is a viable alternative to their fossil fuel comfort blanket. In the construction, agriculture, and mining (CAM) industries, electrification is an even steeper uphill battle. In these industries, if a machine runs out of battery, the operators will soon start losing money. Moreover, these industries have a broad spectrum of machines, each with unique use cases. IDTechEx's new report, "Battery Markets in Construction, Agriculture & Mining Machines 2024-2034", showed that CAM machines require a diverse range of battery solutions to cater to their individual needs. This is especially true of agriculture machines, i.e. tractors.

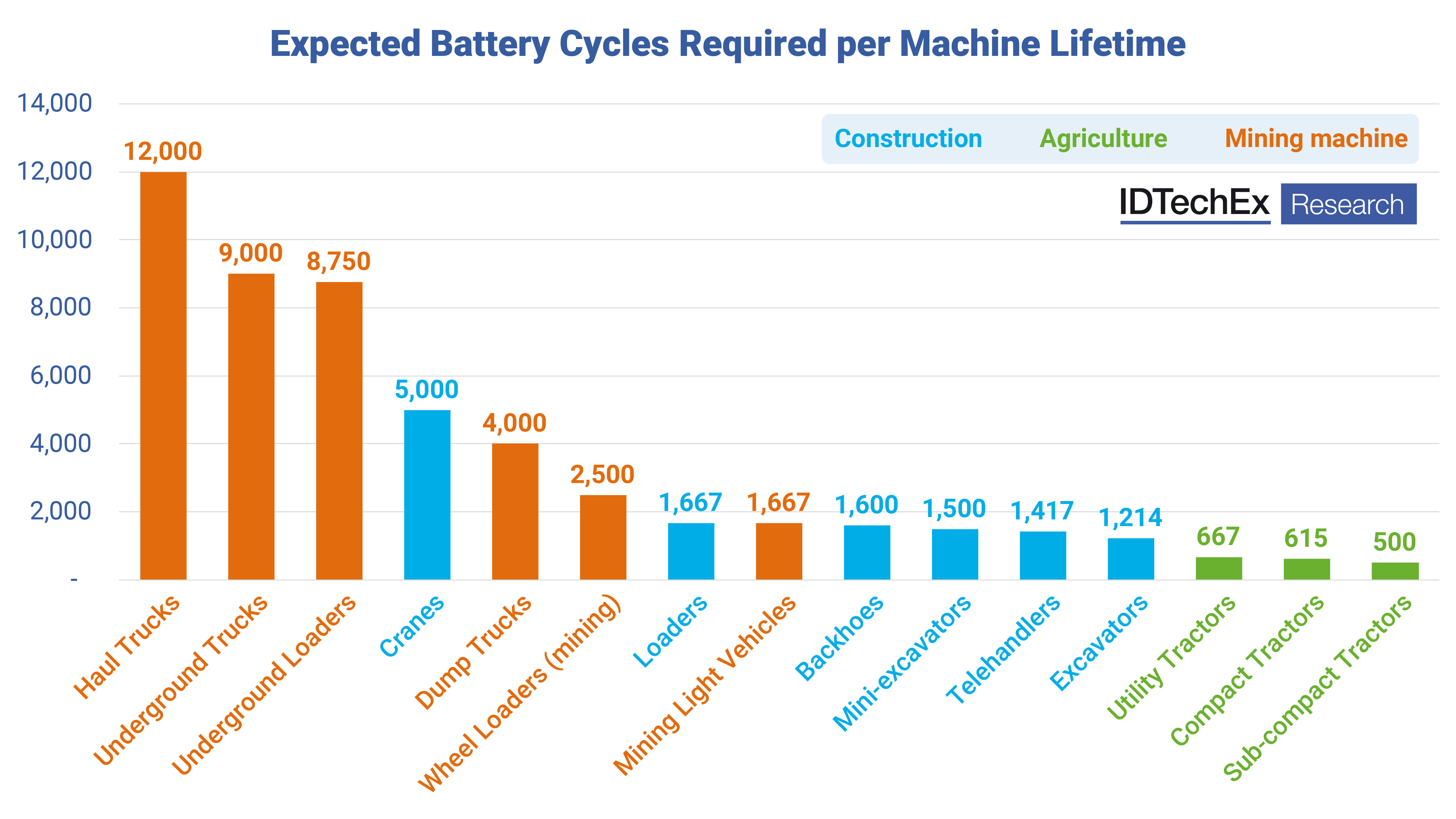

Expected battery cycles required per machine lifetime. Source: IDTechEx

It is likely underappreciated just how unique a challenge the electrification of tractors presents. The first challenge is that their use case is incredibly energy-intensive. For the most part, the purpose of a tractor is to drag machinery through a field. Sometimes, this work is low intensity, such as mowing grass in large fields. Here, the mower attachment isn't too heavy and creates little resistance with the ground. On the other hand, plowing a field creates lots of resistance and, therefore, uses lots of energy. Additionally, if a field has soft mud, the tractor will lose energy due to the tires slipping.

As an example of how much energy tractors consume, a 14-tonne tractor would typically use an engine with around 300hp (maximum), and it can expect to burn around 50L/hr in fuel. For comparison, a 14-tonne excavator would typically use an engine with 120hp and expect to burn around 10-12L/hr in fuel. So why the big difference? Both machines have hard and similar workloads; the tractor could be pulling a plow through the mud while the excavator is removing large quantities of material with its bucket. The key difference is that the excavator is at its peak load only momentarily as it breaks through the ground. The rest of the time is spent raising the bucket above the ground, twisting, dumping the load, then repositioning. The tractor, on the other hand, is working at a constant near-peak capacity. From a battery standpoint, this means that the tractor needs substantially more storage to give the same run time.

The second challenge for electrifying tractors is chassis size. While large construction machines have large chassis to incorporate the battery, tractor chassis are a little more compact, even large 14-tonne ones. Additionally, large excavators can handle the weight of the battery, with many already having concrete ballasts for balance. Excessive weight could be an issue for tractors, especially when operating in wet mud. Moreover, tractors are more sensitive to the location of the weight, preferring an even weight distribution across the wheels for the best stability in the mud. So, not only do tractors need more battery power per hour than other similarly sized CAM machines, but they also have tighter constraints on where that battery can go.

The third challenge with electrifying tractors is their uptime. Again, this is an area where tractors are particularly unusual. Construction and mining machines tend to be in almost constant use, but many tractors have very seasonal work. They could sit dormant for large portions of the year, but come harvesting time on a large farm, they could be running 24/7 for days at a time. In some ways, this is both a blessing and a curse. High uptime in peak season means that the battery needs to be capable of rapid charging to minimize downtime. This is typically tough on batteries, as regular fast charging can degrade their cycle life. However, the blessing is that sporadic usage means fewer cycles are needed over a vehicle's lifetime. Many tractors have life expectancies of around 2,000-5,000 hours, whereas large excavators might operate more than 10,000 hours over their life span. A shorter life expectancy, with fewer cycles required, opens up battery options to more cutting-edge and emerging technologies.

Considering how and when tractors get used, the three key challenges for electrifying tractors can be summarized as:

1) Needing high installed energy capacity to deal with the intensive workload

2) Having limited space, and constrained conditions for the battery installation

3) Needing very quick recharges to minimize downtime in peak season

Today's dominant battery technologies are NMC and LFP, used almost ubiquitously throughout the automotive industry. NMC offers good energy density but typically recharges slower compared to LFP. LFP has compromised energy density but is cheaper and can be recharged more quickly. Both have plenty of cycle life for agricultural applications, but IDTechEx suggests that other emerging options with higher energy density could offer a better fit.

Solid-state batteries (SSBs) and silicon anode batteries are two emerging technologies that might work well in tractors. Both offer improvements in energy density when compared to NMC and LFP, making it easier to put more kWh of battery capacity onto the tractor. Both offer good to high recharging performance, minimizing downtime. Finally, both offer the equivalent or higher safety than LFP and NMC. Unfortunately, both technologies are also very new, still in the early stages of commercialization, and therefore are very expensive.

Electrification is already an expensive endeavor, with the battery being the costliest factor and creating the bulk of the price premium associated with electric alternatives. IDTechEx has seen batteries as large as 1,000kWh proposed for electric tractors. Using NMC or LFP technologies would cost in the region of US$300,000, and with SSB and silicon anode technologies, this could be doubled or even tripled. The battery would likely exceed the cost of a regular diesel tractor of the same size. Even with a tractor this size burning in the region of US$30,000 worth of fuel each year, it is unlikely that the extra cost of an SSB or silicon anode battery could be recuperated.

Solid-state batteries and silicon anode batteries make a good fit for agricultural machines from an engineering perspective, but unfortunately, they don't quite make the business case, for now. As such, IDTechEx's report "Battery Markets in Construction, Agriculture & Mining Machines 2024-2034" forecasts that SSB and silicon anode will have a small market share of battery demand for agricultural vehicles once they are more mature, but demand will still be dominated by NMC and LFP, even in 2034.

The report from IDTechEx considers a total of 15 machine types across construction, agriculture, and mining, evaluating the needs of each and matching them up against ten existing and emerging battery technologies. For a comprehensive guide to the battery markets for electric CAM machines, visit www.IDTechEx.com/CAMBatteries to find the full report. Downloadable sample pages are available for this report.

For the full portfolio of batteries and energy storage market research from IDTechEx, please visit www.IDTechEx.com/Research/ES.

About IDTechEx

IDTechEx provides trusted independent research on emerging technologies and their markets. Since 1999, we have been helping our clients to understand new technologies, their supply chains, market requirements, opportunities and forecasts. For more information, contact research@IDTechEx.com or visit www.IDTechEx.com.