IDTechEx forecasts that the Li-ion battery cell market will reach over US$400 billion by 2035 in the new market report, "Li-ion Battery Market 2025-2035: Technologies, Players, Applications, Outlooks and Forecasts". While there has been strong growth in the stationary battery sector, electric vehicles remain the key driver behind the Li-ion market, and electric cars will be the largest market for Li-ion batteries over the next 10 years. Although there are some regional concerns over the rate of EV adoption in 2024, sales of electric vehicles grew rapidly in 2022 and 2023, and the medium-long-term outlook for EV adoption remains strong. 2023 and 2024 have also seen substantial declines in battery prices, driven by lower raw material prices, production overcapacity, and strong competition throughout the supply chain. While this is beneficial to consumers, it has also impacted margins and exacerbated the difficulty of new entrants succeeding in the Li-ion market.

Cell manufacturing and the Li-ion market

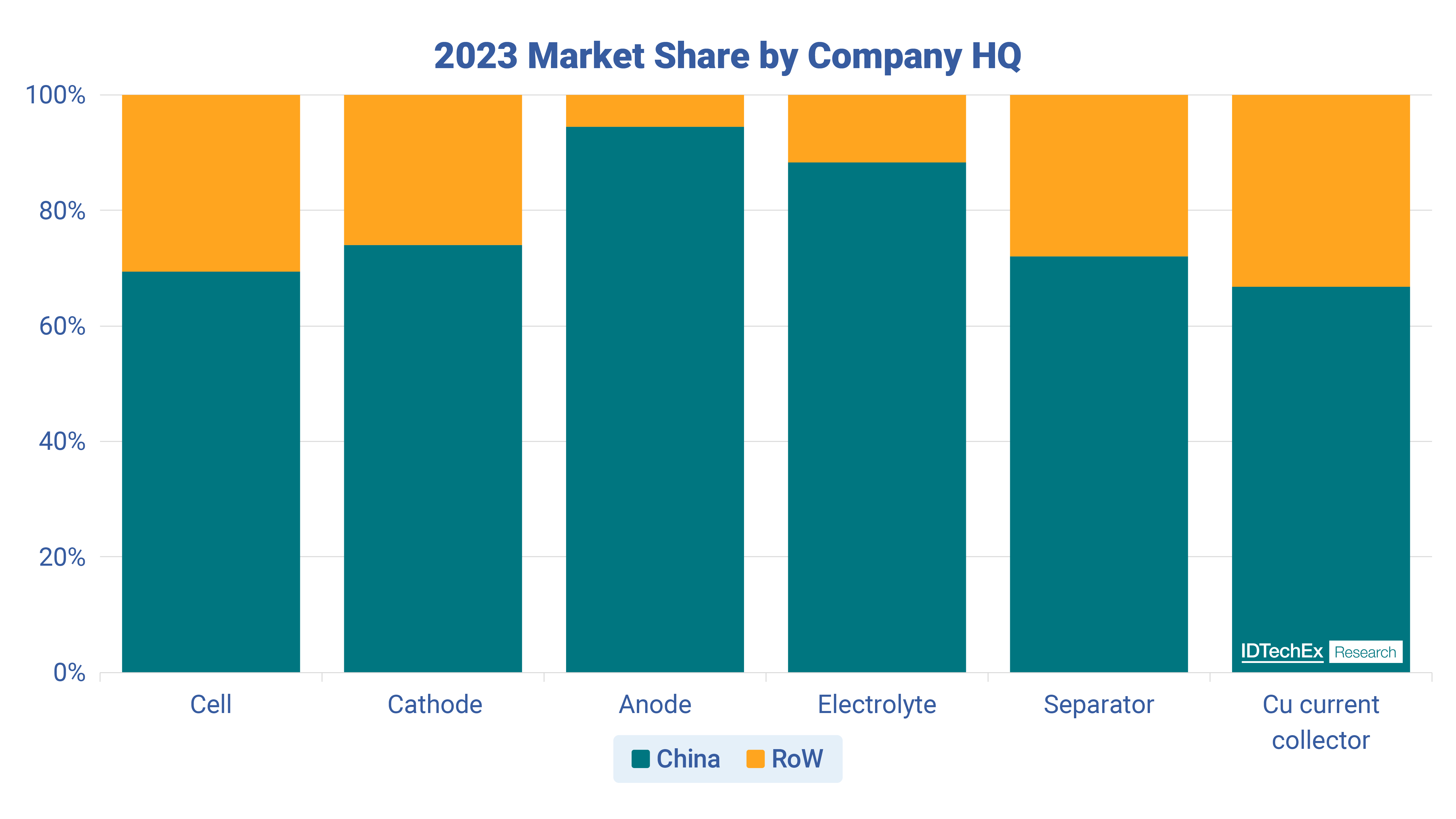

Given the rapid increase in forecast demand for Li-ion batteries over the past 5 years, there has been significant growth in the number of gigafactories brought online as well as those being planned and announced. Much of this has been driven by incumbent manufacturers such as CATL, BYD, LG Energy Solution, SK Innovation, and Samsung SDI, along with a number of fast-growing Chinese manufacturers. IDTechEx estimates that the majority of cell production is located in China, a trend common across the Li-ion value chain where Chinese companies control much of the market for anodes, cathodes, electrolytes, separators, and copper current collectors.

Chinese companies control much of the Li-ion supply chain. Source: IDTechEx

To reduce reliance on a single region and develop domestic battery manufacturing capabilities, Europe and North America are attempting to foster domestic supply chains. In the US, the Inflation Reduction Act (IRA) announcement led to a flurry of gigafactory and investment announcements. Prior to the IRA, IDTechEx estimated that approximately 600 GWh of battery cell capacity would be located in North America by 2030 with this figure growing to 850 GWh in IDTechEx's latest analysis. In Europe, the reality of scaling production rapidly, competing with established Asian players, and some slower than expected demand has inhibited recent investment and expansion plans. Challenges remain in establishing robust battery supply chains in America and Europe.

Anodes and cathodes

The anode and cathode materials, which ultimately define the performance of a Li-ion battery, continue to evolve. At the cathode, a shift toward LFP has been driven by China and a broader attempt to bring down battery price points. Numerous battery manufacturers and automotive manufacturers outside of China are now looking to develop LFP-based batteries or other low-cost solutions. Nevertheless, the high energy density of high-nickel NMC / NCA / NCMA type cathodes means it will remain a key chemistry for long-range and performance-oriented electric vehicles or other applications requiring high energy densities and long runtimes. In line with the broader market, cathode prices, including for LFP and NMC materials, have fallen substantially from early 2023 due to sharp reductions in lithium and raw material prices, as well as overcapacity and competition.

At the anode, new materials, especially silicon-oxide and silicon-carbon composites, continue to garner interest due to their potential to improve energy density despite issues regarding cycle life and lifetime. The potential to establish supply chains for silicon anodes outside of China represents another potential benefit, with anode production particularly concentrated in the region. While excitement builds for new anode materials, graphite remains the dominant material used for Li-ion anodes. IDTechEx estimates close to 99% of total anode material used in Li-ion batteries is graphite.

Applications and markets

Battery electric cars have been one of the key drivers behind growth in Li-ion demand over the past 10 years and are forecast to remain the dominant driver of Li-ion battery demand. Developments and innovations continue to be made in Li-ion anode and cathode materials, manufacturing, cell design, and pack design, all contributing to improved performance and price points and the general positive outlook for EVs. However, significant opportunities exist in other applications and markets. These include a variety of different vehicle classes, from large electric trucks and mining vehicles to electric 2- and 3-wheelers, through to grid-scale and residential battery energy storage systems, each with their own performance priorities, not all of which can be satisfactorily met by current generation batteries. The stationary sector has seen rapid year-on-year growth due to increased deployment of renewable energy onto electricity grids and particularly fast drops in stationary battery prices. Longer lifetime and higher capacity containerized storage systems offer a glimpse into the continued innovation going into Li-ion battery systems.

To find out more on the status of the Li-ion battery market, key players, technology developments and trends, battery price analyses, and developments in battery markets and applications, see the new IDTechEx report "Li-ion Battery Market 2025-2035: Technologies, Players, Applications, Outlooks and Forecasts".

Key aspects of this report include:

- Analysis and discussion of Li-ion materials, technologies, and market trends

- Status of Li-ion cathodes and anodes, including key companies, production expansions, chemistry trends (NMC, NCA, NCMA, LFP, LNMO, LCO, natural graphite, synthetic graphite, silicon).

- Battery production and capacity outlooks. Status of Li-ion global and regional cell manufacturing capacity and expansions.

- Analysis of key players across cell, cathode, anode, electrolyte, separator and current collector producers.

- Status of Li-ion electrolytes, separators, current collectors, and conductive additives

- Li-ion cost and price analysis and forecast.

- Forecast of Li-ion battery demand by application and chemistry.

Upcoming free-to-attend webinar

Insights on the Li-ion Battery Market: Opportunities and Challenges Ahead

Dr Alex Holland, Research Director at IDTechEx and author of this article, will be presenting a free-to-attend webinar on the topic on Thursday 26 September 2024 - Insights on the Li-ion Battery Market: Opportunities and Challenges Ahead.

This webinar will cover:

- Recent trends and developments in the Li-ion market

- Discussion on various chemistry choices being made

- Key technology innovations and developments

- Cost and price trends

We will be holding exactly the same webinar three times in one day. Please click here to register for the session most convenient for you.

If you are unable to make the date, please register anyway to receive the links to the on-demand recording (available for a limited time) and webinar slides as soon as they are available.

About IDTechEx

IDTechEx provides trusted independent research on emerging technologies and their markets. Since 1999, we have been helping our clients to understand new technologies, their supply chains, market requirements, opportunities and forecasts. For more information, contact research@IDTechEx.com or visit www.IDTechEx.com.