Li-ion batteries continue to be the default secondary battery option for many applications and markets, ranging from small electronic devices to various types of electric vehicle, through to large grid-scale stationary battery systems. The Li-ion industry continues to innovate to reach higher energy densities, faster charge and higher rate capabilities, longer lifetimes, lower costs, and lower environmental impact from their production to better meet the demands of the markets and applications reliant on battery and energy storage technology.

Energy density- silicon anodes a key lever for energy density improvement

Energy density remains a critical performance metric. Improving energy density can increase the range of electric vehicles, improve the runtime and functionality of electronic devices, or enable electric aviation.

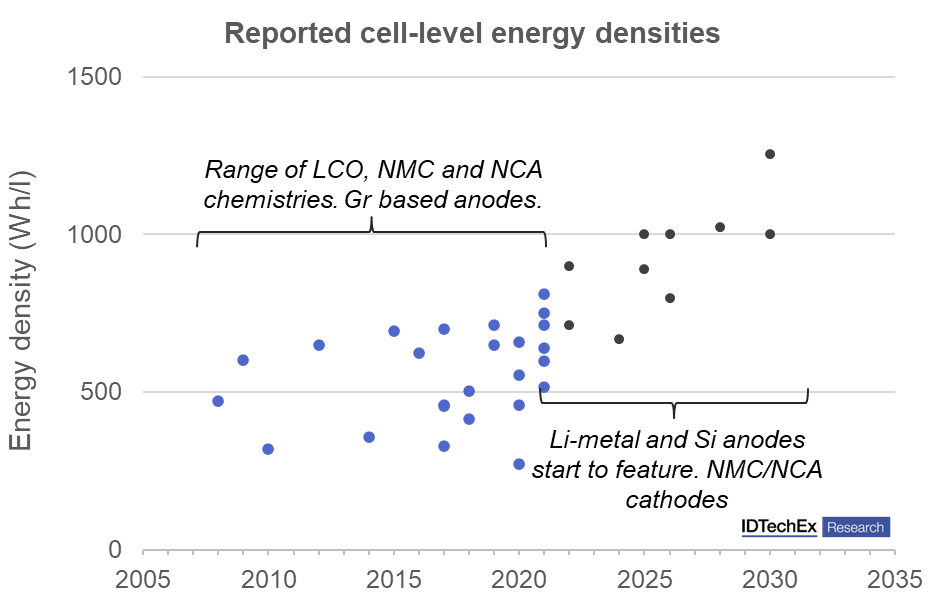

Graphite is the most widely used anode material. The use of graphite enables cells with energy densities of 250 Wh/kg and 650 Wh/l when coupled with NMC or NCA cathodes in well-designed cells. Numerous battery electric cars are able to advertise ranges of 400 miles using cells with this level of energy density, but ICE cars can reach 600+ miles. Silicon anodes can feasibly increase the energy density of Li-ion batteries by 50% in the long term due to its theoretical capacity being 10x that of graphite. In the short-medium term, more modest improvements are expected.

Silicon is already used as an additive at <10% in some batteries, but increasing the percentage of silicon beyond this has proved challenging due to its large volume expansion, leading to short cycle lives and lifetimes. However, multiple solutions are under development that can enable the utilization of higher percentages of silicon, ranging from silicon-carbon composites, nanostructured silicon material, and innovative electrolyte, electrode, and cell designs.

Start-ups such as Group14 Technologies, Nexeon, and Sila Nano, amongst others, are building production facilities with the aim of deploying material commercially, at scale, over the next 2-3 years. Major anode material producers such as BTR and Shanshan are expanding their silicon anode production capacities, while other established materials companies are also investing in their capabilities, highlighting an increasing expectation for deploying more silicon material into Li-ion batteries.

Figure 1. Reported energy densities of commercial and prototype Li-ion cells.

Lithium metal offers an alternative high energy density material with a similarly high capacity to silicon. Anode-free designs present another interesting development, offering the opportunity for effectively maximizing energy density and minimizing anode material cost. Issues regarding low efficiency and lifetime of lithium metal anodes are exacerbated with anode-free designs. Nevertheless, companies such as Samsung SDI intend to develop anode-free solid-state batteries, whilst Our Next Energy plans to use anode-free cells in combination with long life LFP in the hybrid battery packs.

Beyond the anode materials, various other cell and pack design optimizations, including maximizing cathode voltages and capacities, thinner current collectors, cell-to-pack designs, and numerous other design considerations, will help maximize battery energy density.

Improving safety and longevity

With some high-profile recalls and ongoing concerns about the safety of battery systems, especially in vehicles and stationary applications, the safe operation of Li-ion batteries has become critical. Solid-state batteries have been one of the main pillars of next-generation battery development. This stems from their potential to improve both safety and energy density by replacing the flammable and volatile organic electrolyte with a more stable solid electrolyte, which can also allow for the use of lithium metal anodes. However, promises of commercialization have been slow to realize. Several manufacturers are targeting 2027/28 for mass production and commercialization, but a history of delays in the deployment of solid-state batteries highlights the associated risks and challenges.

In China, there has been a focus on semi-solid state batteries where composite liquid/polymer electrolytes are being developed in a bid to provide some of the safety and longevity benefits of solid electrolytes while retaining the manufacturability of existing liquid electrolyte cell designs. WeLion are a prominent example who have shipped cells to EV manufacturer Nio. Their patents suggest the use of composite, in-situ polymerized electrolytes to enable the use of polymer electrolytes over the full voltage window of a Li-ion battery while maintaining a similar manufacturing process to current batteries.

The "zero-degradation batteries" advertised by CATL for their stationary systems brought long-cycle life batteries back into the limelight after previous announcements and developments into "million-mile" EV batteries. Cycle life and lifetime are particularly important for commercial electric vehicles and stationary storage systems where warranty provision, total cost of ownership, and levelized costs are primary considerations. Zero-degradation claims and long-cycle life characteristics can be enabled by lithium supplement cathode additives such as Li5FeO4, suitable electrode and cell design, and various electrolyte additives and formulations, highlighting the ongoing developments in liquid electrolytes.

Battery management systems are also playing a more important role in maximizing battery performance, becoming more intelligent to safely enable longer lifetimes, faster charging, early fault detection, or to minimize charge/discharge profiles and modes of operation that lead to accelerated degradation. Thermal management systems are also shifting in design. One major change is the application of thermal interface materials (TIMs), pushing in favor of thermally conductive adhesives to make a structural connection rather than the typical gap filler seen in many existing designs. Many material suppliers are tailoring their materials to provide multiple functions, including fire protection, enabling fire protection to be included without severely impacting the energy density of the pack.

Fast charge capability in focus

Battery manufacturers and automotive OEMs are increasingly highlighting the importance of fast charging capability (down to 10-minute charge times) as a performance metric for electric cars and vehicles. Beyond the inherent benefits of high-rate capability, this is further driven by the increasing difficulty and cost of increasing energy density while maintaining cycle life and safety. Fast charge capability will also be valued in applications, including power tools, cordless appliances, and consumer electronics devices.

For example, CATL released their 4C LFP battery. Samsung SDI are targeting 0-80% SOC in 9 minutes by 2026. SK On are targeting 15 minute charge times by 2026 and a 10 minute fast charge capability by 2030, representing the addition of 300 km range in 5 minutes. Multiple design levers are being pulled to enhance fast charge capability, from using additional conductive and porous silicon anode material, multi-layer electrodes, optimized material distribution within electrodes, thermal management, and adaptive charging protocols.

Material costs and competition drive down prices

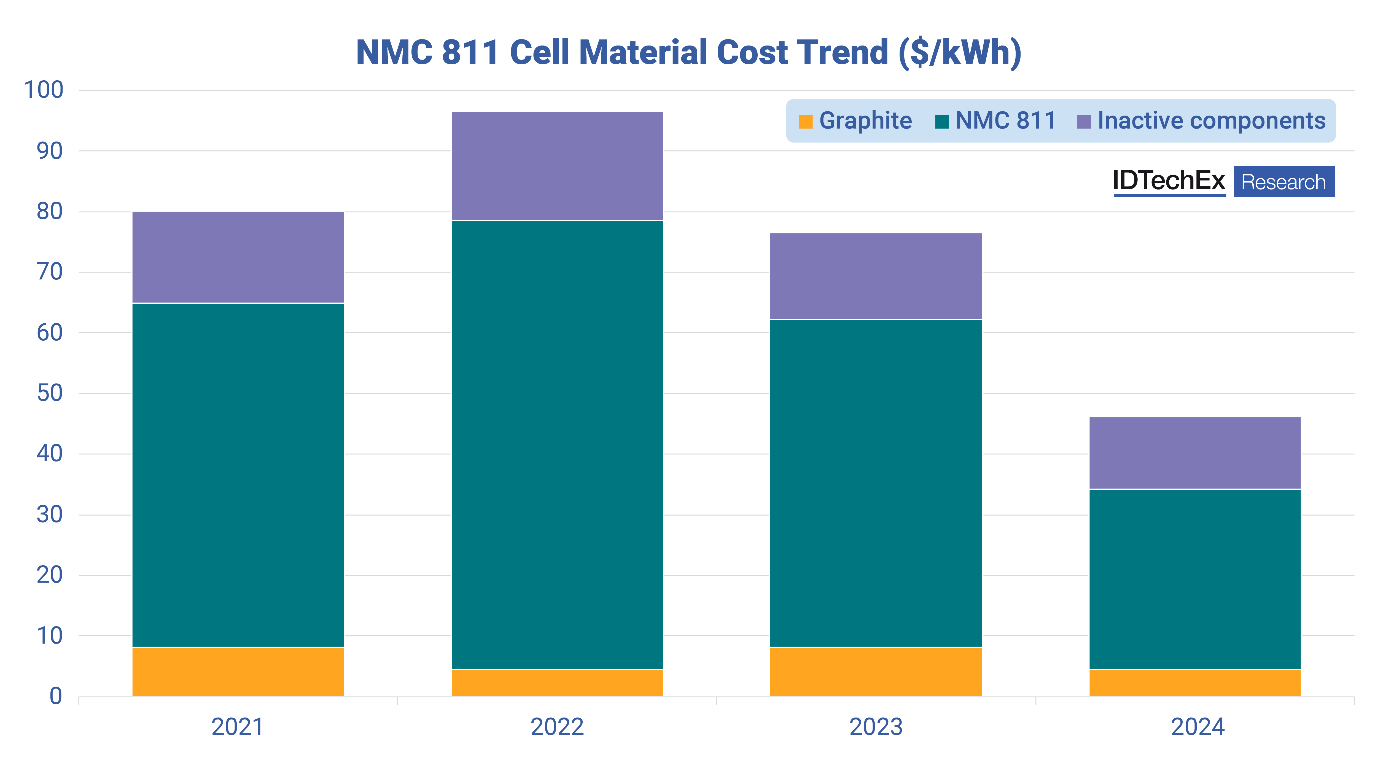

Cathode materials are a key contributor to overall cell and battery costs. The shift toward LFP has largely been driven by increasing cost pressures. However, while LFP offers a distinct cost advantage over NMC and NCA, it also suffers from lower energy densities. New cathode materials aim to minimize this trade-off. For example, the higher average voltage of LMFP results in an energy density increase compared to LFP, whilst maintaining a similar cost. Other options for minimizing the trade-off between LFP and higher energy NMC/NCA include Li-Mn-rich and high-voltage LNMO. Of course, the low material prices and extensive competition in the market highlight how cost benefits can be highly dependent on shifting material prices and market dynamics.

Figure 2. Cell and material prices have dropped significantly since 2022. The cost of the cathode still contributes a significant percentage to cell material cost and, therefore, cell prices.

2024 has seen sharp drops in anode, cathode, and cell prices, amongst other components. This has been driven by a combination of factors, including declines in raw material prices, production overcapacity and strong competition, lower-than-expected demand in Europe and North America, and process innovations. Drops in prices have typically been coupled with drops in margins, highlighting the difficulty of competing in this market as a new entrant.

Li-ion battery technology is not standing still; it is subject to continued development and innovation, which will help to improve performance, enhance safety and longevity, reduce costs, and minimize environmental impact. Despite ongoing interest in alternative battery technologies, from Na-ion to redox flow batteries, Li-ion batteries will remain the dominant rechargeable battery technology across important end sectors such as electric vehicles and stationary energy storage systems.

To find out more about the Li-ion battery market, innovations and developments in battery technology, or developments in non-lithium batteries and markets, IDTechEx offers a wide portfolio of research delivered through market reports and subscription services - visit www.IDTechEx.com/Research/ES for the full list of available reports.

Technology Innovations Outlook 2025-2035

This article is from "Technology Innovations Outlook 2025-2035", a free collection of insights from industry experts highlighting key technology innovation trends shaping the next decade. You can download the full collection here.

About IDTechEx

IDTechEx provides trusted independent research on emerging technologies and their markets. Since 1999, we have been helping our clients to understand new technologies, their supply chains, market requirements, opportunities and forecasts. For more information, contact research@IDTechEx.com or visit www.IDTechEx.com.