Global battery energy storage system (BESS) deployments continue to be deployed at a rapid pace, with surging deployments seen especially in grid-scale markets. Giant Li-ion BESS players dominate this market leaving untapped opportunities for smaller players to exploit in commercial and industrial (C&I) sectors, behind-the-meter (BTM). However, operating in this underappreciated market can be complex, given the vast end-use applications and changing regional drivers. This article highlights the emerging demand for C&I BESS technologies.

As the volume of renewable energy sources penetrating electricity grids continues to increase, as will the demand for grid-scale battery energy storage systems (BESS). Key Li-ion BESS players have continued to dominate the grid-scale energy storage (ES) market. However, this has created opportunities for smaller players to grasp in untapped commercial and industrial (C&I) energy storage markets.

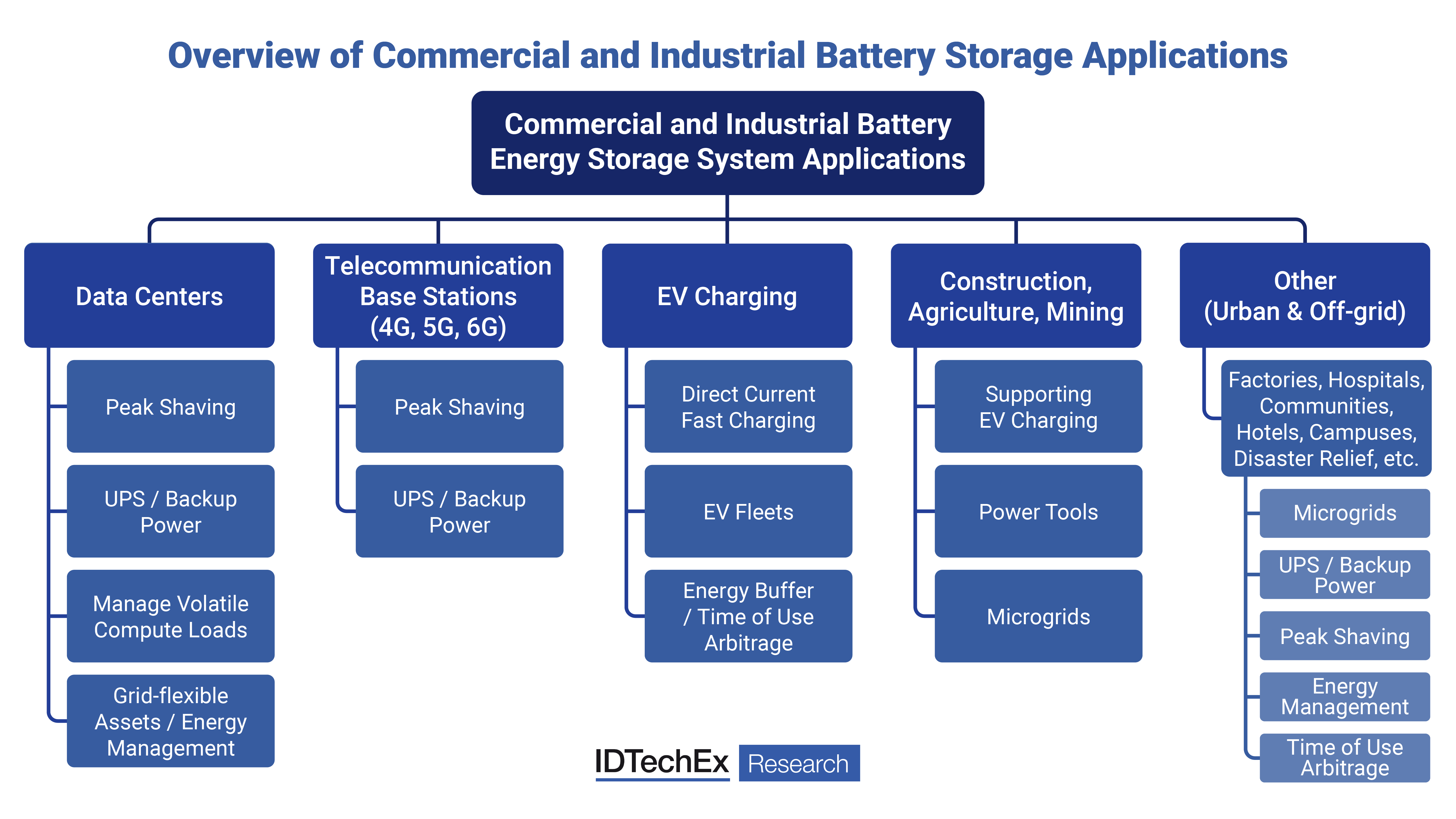

These opportunities will continue to both grow and shift across a range of sectors, including data centers, telecommunication towers, and supporting electric vehicle (EV) charging in both on-road and off-road segments such as construction, agriculture, and mining. Across these applications, and as shown in IDTechEx's new market report "Battery Storage for Data Centers, Commercial & Industrial Applications 2026-2036: Market, Forecasts, Players, Technology", the commercial & industrial battery storage market is predicted reach US$21B in value by 2036.

For this value to be realized, technology developers will have to adapt to shifts in application demand, and end-user requirements which consider battery storage cost, safety, and degradation, among other factors. This market is complex, constantly transforming, and the battery storage technologies adopted may also evolve over time.

Overview of commercial and industrial battery storage applications. Source: IDTechEx.

C&I BESS Demand: Sectors and Regions

Demand for C&I BESS is set to grow significantly in-line with data center rollout, especially in the US. Hyperscale data centers in the GW-scale will start putting strain on electricity grids, and so larger capacity, longer duration battery storage technologies may be needed to provide improved grid flexibility and cover the power demand of the data center over longer periods of any deficits in electricity supply.

While demand for battery storage in US data centers is set to increase, the demand for C&I BESS in other applications and regions should not be ignored. For instance, waves of 5G and 6G tower deployment in China, alongside data center rollout and customers looking to adopt on-site storage at private factories in Europe, will transform demand for C&I BESS over the coming decade.

In the mid-2030s, global demand will also shift outside the US and Europe, where C&I BESS is expected to support charging of electrified machines in construction and agriculture sites. IDTechEx's market report provides 10-year market forecasts and a market analysis on how application demand will grow and change in these various regions, while also investigating individual players operating in the market.

C&I BESS Technology Trends

Li-ion BESS technologies have dominated grid-scale, C&I, and residential battery storage markets. With the growing demand for C&I BESS in the US, especially for data centers, it is critical for many in the Li-ion value chain to understand the potential cost differences in importing Chinese LFP Li-ion cells, vs manufacturing these domestically in the US. This market report from IDTechEx provides a clear, quantitative analysis of these Li-ion cell cost differences in 2026, which considers Li-ion tariffs, tax credits, foreign entity of concern (FEOC) restrictions, and material assistance cost ratio (MACR) thresholds, as well as Li-ion C&I BESS cost by component breakdown and US LFP cell manufacturing plants being planned.

Despite the dominance of Li-ion BESS, its flammability and cell degradation poses key disadvantages which may render them less safe or practical in certain C&I applications. In data centers, for instance, managing volatile MW-scale compute artificial intelligence (AI) loads can cause more rapid Li-ion battery degradation than the Li-ion BESS technologies deployed on the grid; Li-ion technologies in data centers may be cycled more frequently. Other technologies such as redox flow batteries (RFB), which exhibit minimal degradation over 20,000+ cycles and non-flammable electrolyte, could be deemed a more suitable technology fit.

As well as RFB developers, sodium-ion, second-life EV, and valve-regulated lead acid (VRLA) battery technology developers will all have their parts to play with advantages which they can leverage from their respective technologies. IDTechEx's new market report provides an in-depth analysis and outlook on battery storage technologies for C&I applications, and benchmarks these technologies against Li-ion, across Capex for C&I systems and key technical metrics.

In the new market report, "Battery Storage for Data Centers, Commercial & Industrial Applications 2026-2036: Market, Forecasts, Players, Technology", IDTechEx brings the reader a holistic overview of this market, including the following information:

Market Forecasts and Analysis

- Granular 10-year C&I BESS market by region (GWh), by application (GWh) (data centers, 5G telecom base stations, 6G telecom base stations, EV charging, "construction, agriculture and mining", and other), and by value (US$B). 10-year forecasts by application (as above, GWh) per region are provided, and by GW for data centers per region are also provided.

Commercial and Industrial Battery Storage Applications & Global Market

- Analysis on battery storage for key C&I applications, including data centers, 5G and 6G base stations, EV charging, construction, agriculture, and mining (CAM), and other applications.

- Deep dive into the global C&I battery storage market, featuring research from dozens of primary interviews conducted across regions between IDTechEx and key players, providing unique insights into this market for the breadth of applications covered.

- Key battery storage for data center market developments, including key projects and BESS technologies for data centers.

- Cost benefit analysis of battery storage for data centers, and key commentary on evolving demands of BESS and their technology trends for data centers.

Company Profiles

- 30+ company profiles including C&I BESS players, major Li-ion BESS companies, and players developing alternative battery storage technologies, e.g., redox flow batteries, Na-ion, second-life EV, VRLA, and zinc-based batteries.

Li-ion Technologies and Costs

- Key quantitative analysis and explanations on costs of LFP Li-ion cells in the US vs importing LFP Li-ion cells from China in 2026 with implementation of The One Big Beautiful Bill Act (OBBBA), 45X Manufacturing Tax Credits, FEOC restrictions, MACR thresholds, and tariffs on Chinese LFP cells.

- US LFP cell manufacturing plants for battery energy storage systems (BESS) by capacity, player, location, and status.

- Li-ion C&I BESS cost breakdown by component (cells, fire protection and thermal management systems, power conversion system, battery management system, housing) in 2025 vs 2036, for high power (0.5h) and high energy (4h) batteries.

- Li-ion C&I BESS technology benchmarking between key players' technologies.

Competing Battery Storage Technologies for C&I Applications

- Technology analysis, benchmarking, discussion, and trends of key battery storage technologies specifically for C&I applications, including LFP and NMC Li-ion BESS, Na-ion batteries, redox flow batteries, second-life electric vehicle batteries, and VRLA batteries.

- C&I BESS technology outlook from IDTechEx for the 2025 - 2036 period is also provided, including LFP Li-ion, NMC Li-ion, Na-ion, redox flow batteries, second-life electric vehicle batteries, and valve-regulated lead-acid (VRLA) batteries.

For more information on this report, including downloadable sample pages, please visit www.IDTechEx.com/BS4DC, or for the full portfolio of related research available from IDTechEx, see www.IDTechEx.com.