As the Li-ion battery industry continues its rapid expansion, manufacturers increasingly seek methods for cheaper cell production with improved consistency and performance. The emergence of dry electrode processes is just the latest step in this greater trend, as manufacturers seek to replace the slurry-based production methods widely used today.

IDTechEx's new "Additives for Li-ion Batteries and PFAS-Free Batteries 2026-2036: Technologies, Players, Forecasts" report dives into what these processes are, why they are gaining so much traction, and how their rise will impact the Li-ion binder market. IDTechEx forecasts that the binder market for dry electrode processes will near US$700 million in market value by 2036.

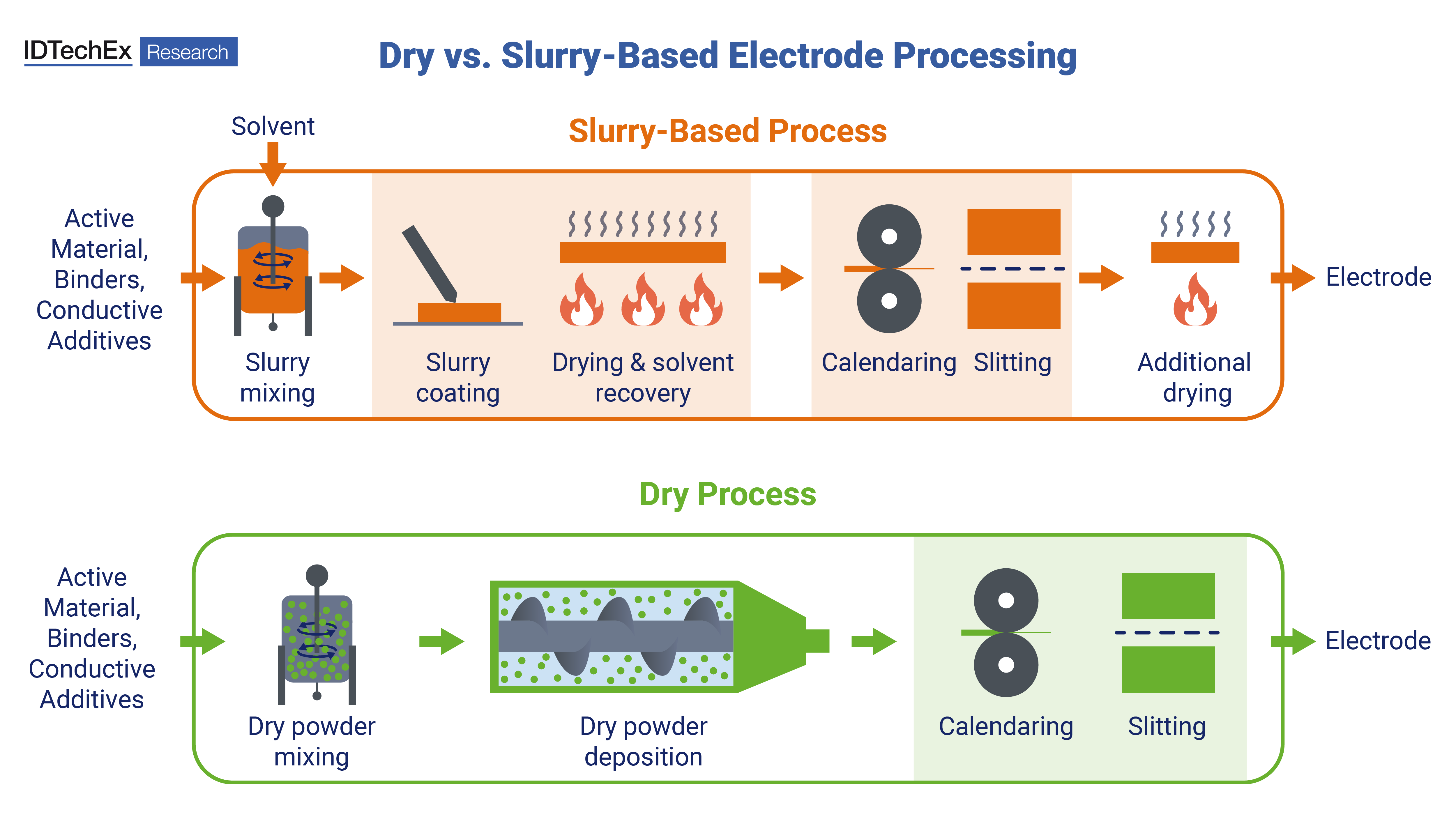

What are dry electrode processes?

The slurry-based electrode production processes widely used today (sometimes referred to as slurry-cast or wet processes) use solvents to form a slurry containing the electrode active materials, binders, conductive additives like carbon black, and more. The slurry is coated onto a current collector before it undergoes thorough drying to recover the solvent, leaving behind a solid electrode that can be calendared and slit into shape. This is sometimes followed by an additional drying step to ensure no solvent makes it into the final electrode.

A dry electrode process, on the other hand, uses no solvent at all. Instead, active materials, binders, and other additives are mixed together as dry powders and can be directly deposited onto the current collector in a number of different methods. This essentially forms the final electrode ready to be calendared, silt, and integrated into the cell. The result, as per the findings of the "Additives for Li-ion Batteries and PFAS-Free Batteries 2026-2036: Technologies, Players, Forecasts" report, is a much shorter production line that is more sustainable and requires far less energy usage.

Dry processes are significantly shorter than slurry-based ones by foregoing solvents entirely and the drying steps that come with them, Source: IDTechEx

Why are dry electrode processes gaining traction?

Dry processes are now an incredibly hot topic within the battery industry, and that is due to all of the potential benefits they can provide. Eliminating solvents and drying steps makes the manufacturing line shorter and take up less space, with reductions in floor area of 75-90% already achievable currently. More significant than the savings in floor space is what can be saved in energy usage. The drying steps within a slurry-based production process are often the most energy-hungry steps within the production line, and eliminating these can save manufacturers more than 50% in energy costs. Combining all these savings creates real potential for battery manufacturers to drive down the prices of their cells at a pivotal time for the global electrification effort.

Additionally, the solvent used in most cathode production is the organic solvent NMP - a material that is uniquely able to dissolve the PVDF cathode binder but is highly toxic, with serious health consequences to people upon exposure or leakage. Most slurry-based processes, therefore, require a high degree of safety and careful material handling to prevent exposure; however, dry processes require far fewer precautions and can reduce the risks to people by eliminating the toxic solvent entirely, creating a more sustainable manufacturing route.

Finally, dry processes can also enhance the performance of cells themselves. The drying steps within a slurry-based process can cause pores and cracks within the electrode, which compromise its strength and compaction. A dry process without drying steps faces none of these issues, resulting in a more energy dense and longer lasting cell. While the performance benefit is admittedly minor, it represents an additional source of improvement for manufacturers which come simultaneously with the enhancements to sustainability and reduced process cost.

It is for all these reasons that, despite dry processes only making up ~1% of global electrode production at the moment, they are the subject of increasing interest and investment within the industry. The new "Additives for Li-ion Batteries and PFAS-Free Batteries 2026-2036: Technologies, Players, Forecasts" report explores key developments in dry processing from major players such as Tesla, LG, and Volkswagen, discussing and contrasting in great detail the independent dry processes each is developing.

How are dry processes shifting the binder market?

There are multiple dry electrode processes currently being explored, with each differing in their dry powder deposition method and the binders they use. A whole gamut of polymers can be used as potential dry binders, ranging from synthetic to bio-based, and novel to commercial.

Fluoropolymers are among the most popular options in the current market. These are materials that most battery manufacturers are experienced with, as PVDF is a fluoropolymer as well. In the dry process market though, PTFE is the dominant fluoropolymer, with one of the key dry processing methods leveraging PTFE's unique fibrillation properties to form an extensive and uniform binding network within the electrode.

PVDF has also been used as a dry binder, though to a lesser extent, while non-fluoropolymer options range from polypropylene and polylactic acid to alternative materials like paraffin wax and rubber-based materials. IDTechEx has laid out which polymers are suited as dry binders in which dry processing methods, and this area of development is likely to be an active one in the coming years with growing research and interest in dry processes as well as the range of processing methods being explored.

"Additives for Li-ion Batteries and PFAS-Free Batteries 2026-2036: Technologies, Players, Forecasts" highlights the seismic shift that dry electrode processes can bring to the battery industry, both in terms of revolutionizing manufacturing and in changing the market for electrode binders. The report analyzes in great detail the multiple types of dry process that are in the midst of commercialization, key players furthering their development, and the binder materials compatible with each process method. This includes in-depth patent analysis as well as discussion of wider market development. Granular 10-year forecasts lay out the growth expected within the dry process market in terms of binder material demand out to 2036.

For more information on this report, including downloadable sample pages, please visit www.IDTechEx.com/AddBatteries. For the full portfolio of battery-related research available from IDTechEx, see www.IDTechEx.com/Research/ES.